Annuity Factor

The annuity factor definition is the use of a financial method that shows the value, present or future, of an amount when it is multiplied by a periodic amount. The calculation of an annuity factor requires the number of years involved, or the periodic amount, and the percentage rate applicable. The most often used for annuity factors are investments with either or both an annual payment or return. Typical examples of annuity factors being applied are savings accounts, certain types of insurances, or retirement savings plans.

The annuity factor meaning is a particular type of accumulating discount factor used to determine the present or future value of annuities, as well as equated installments. Another name for annuity factors is the annuity formula, and we’ll get into that momentarily.

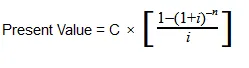

The Present Value Annuity Factor

The present value annuity factor allows you to determine the amount of money required at the present time in order to result in a future series of payments assuming a fixed interest rate is applied.

In order to reach the present value annuity factor, a formula is used that discounts a future value amount to the present value amount through the use of the applicable interest rate. The period of time during which the investment will last is also taken into account to reach the correct value.

The Present Value Annuity Formula

With:

C=cash flow per period

i = interest rate

n = number of payments

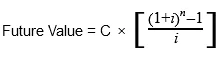

The Future Value Annuity Factor

The future value annuity factor gives access to the final return value of a series of regular investments taking into account their worth at a future time, usually at the end of the investing period, assuming that a fixed interest rate is applied.

To reach the future value annuity factor, the formula above is slightly altered in order to add the values collected over the years by also accounting for the set interest rate.

The Future Value Annuity Factor

With:

C=cash flow per period

i = interest rate

n = number of payments

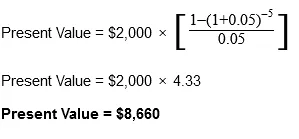

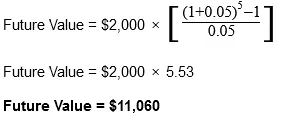

Applying the Annuity Factor formulas:

Considering an investment with an annual $2,000 payment over the course of five years at an interest rate of 5%, let’s see what the present and future value would be.

The previous formulas can help you determine the present and future values of ordinary annuities. While the math might seem complicated, there are financial calculators online that can help you out with the correct inputs and data.

Popular Real Estate Terms

A simple box-shaped house with clapboard siding and a gable roof. ...

Trade group of predominately land developers. ...

Usually a fairly large site zoned and planned for the purpose of industrial development and located outside the main residential area of a city. Industrial parks normally are provided with ...

Putting a waterproofing substance on the exterior cement walls of the structure to prevent water from entering the interior of structure. The cracks in the walls are patched up. ...

Involves more than one borrower being responsible for a mortgage, such as with a cooperative apartment. Involves more than one mortgagee lent on a real estate project, such as with a ...

The basic definition of an acquisition loan is the kind of loan that gives a company the funds necessary to make a purchase. The type of investment depends on the company’s activity, ...

Registered real estate broker who charge a flat fee, rather than a commission, for real estate purchase and sale transactions regardless of the property's sale price. No fee is charge if ...

Worth of the property part which is left subsequent to a condemnation action. ...

The definition of abatement is a reduction of penalties or a tax deduction for individuals or businesses. It can often be accessed upon an overpayment of taxes, if the company or individual ...

Have a question or comment?

We're here to help.